The shares of Life Insurance Corp. of India (LIC) have experienced a modest 2% increase after the announcement of its March quarter results. While the results had some positive aspects, they were insufficient to provide the much-needed boost to the stock.

LIC’s annualized premium equivalent (APE), a crucial measure of growth for insurance companies, rose by 12% year-on-year in the March quarter. However, certain private competitors outperformed LIC in this regard. For example, ICICI Prudential Life Insurance Co. achieved a 26.5% APE growth.

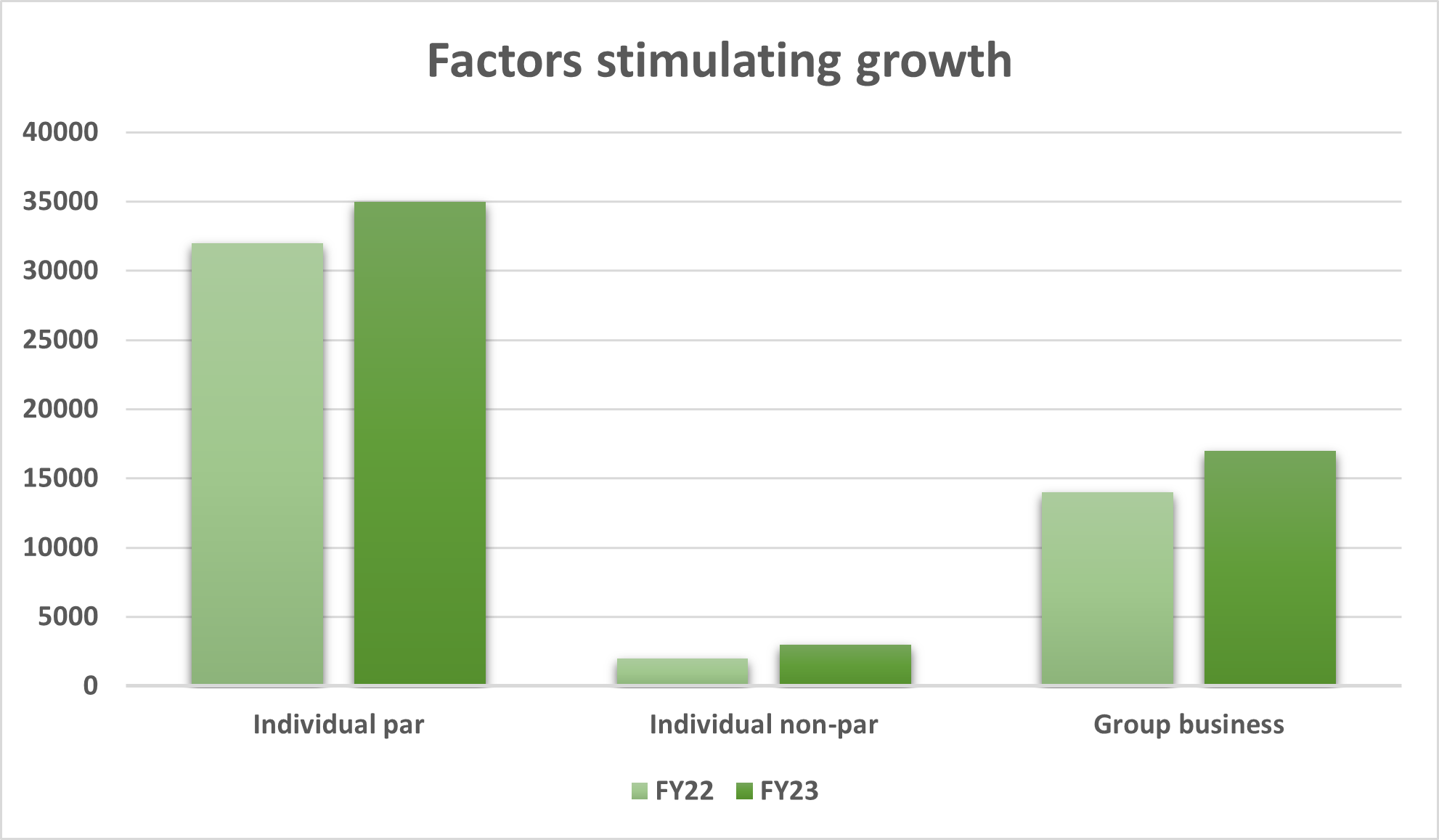

During the March quarter, LIC’s growth in the group business APE was subdued, although management expects improvement in the future. Nonetheless, LIC performed well in terms of margins last quarter due to a product mix that favored high-margin categories, thereby enhancing the value of their new business (VNB) margin. The calculated VNB margin increased by approximately 470 basis points sequentially, reaching 19.4%. While this margin improvement is reassuring, its sustainability requires careful monitoring.

In FY23, the VNB margin stood at 16.2%, up from 15.1% in FY22. However, LIC’s APE growth of 12.5% for FY23 lags behind the industry’s growth rate of 19%. Consequently, there has been a decline in LIC’s market share from 44.0% in FY22 to 41.8% in FY23, according to analysts at JM Financial Institutional Securities Ltd. The analysts also noted that although the LIC management remains confident about regaining the lost market share, this decline has been a concern for investors in the LIC stock and will continue to be closely monitored.

During its earnings call, LIC’s management emphasized its focus on achieving profitable growth in market share. The insurer is taking steps to revitalize its share of non-participating (non-par) products while not neglecting the participating (par) business. The share of margin accretive non-par products increased to 8.89% in FY23 from 7.12% in FY22. Enhancing the proportion of non-par products in the overall portfolio is expected to contribute to LIC’s profitability.

However, the road ahead is challenging. The impact of changes in taxation on large-ticket policies is yet to be seen for all life insurance companies. As expected, FY24 has begun on a weak note for the sector, given the high base of FY23, with LIC trailing behind private competitors. In April, retail APE declined by 2.5% for the life insurance sector, with private insurers and LIC experiencing drops of 1% and 5% respectively.

“On a four-year CAGR basis, the impressive 13% growth for private players contrasts with LIC’s muted 2.5% growth,” according to analysts at Emkay Global Financial Services. Overall, analysts anticipate single-digit retail APE growth in FY24 for the life insurance sector, given the supernormal base of FY23.

Nonetheless, the valuation of LIC stock presents a silver lining as it remains reasonable. Over the past year, the stock has depreciated by approximately 25% of its value. Analysts from Motilal Oswal Financial Services stated in a report on May 25 that LIC stock is trading at 0.6 times FY24E embedded value, considering the gradual recovery in margins and diversification of the business mix.

“Despite expansion, LIC’s VNB margin will still be around half that of top private peers; therefore, we expect the valuation gap to sustain,” said the analysts from Motilal. The brokerage firm believes that a stronger-than-expected growth in non-par savings and protection could lead to a faster normalization of margins and a narrowing of the valuation gap.

Considering LIC’s extensive scale of operations, their successful execution remains crucial.

Disclaimer: We do not endorse or encourage you to take trades or investment decisions based upon our posts/research, all of your trading and investment activities are your own and should be taken through consultation with reputed financial advisors. The analysis posted on this website has been created by involving multiple mediums which are present over the Internet.