Short term unreliability could affect technology sales therefore it might affect the prosperous aspects of TCS, but the long-term saga remains intact.

During a very concerning period of the IT services industry along with the macro turmoil affecting the western markets, TCS performed a comparatively strong show which came out as a surprise. We may expect positive stock reactions because the stock has been oversold in the recent short term. TCS is down by 4.5 percent in the last three months versus a 1.2 percent downfall in the IT Index and over 6 percent rally in the NIFTY index. We should note that TCS has fallen over 20 percent in the last year. The company has given out a decent revenue and margin performance as well as a healthy sales growth in Q2 in spite of the diminishing supply crunch.

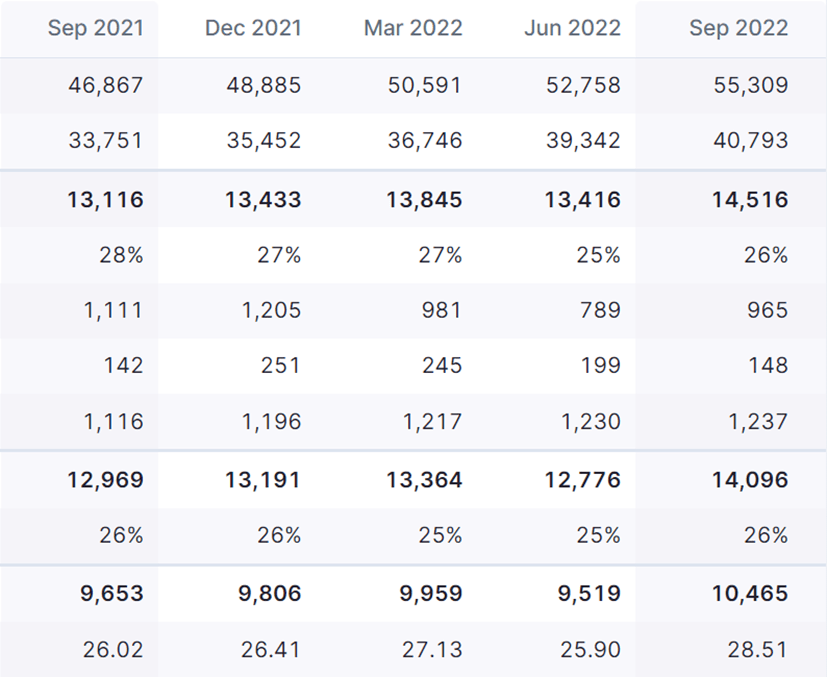

Q2 2022 Earnings Results

TCS reported a revenue of $6877 million in Q2 FY23. Growth was diminished 1.4 percent sequentially as the dollar-rupee currency fluctuations; however, the constant currency sequential growth of 4 percent was healthy. The year-on-year growth in constant currency was 15 percent.

The main markets of North America, Europe and the UK, which together form almost 83 percent of the revenue, have grown YoY in good double digits in constant currency terms. All the seven industry verticals have shown positive YoY growth with a fantastic performance from retail, communication, and manufacturing. Considering the entirety, the existing macro concerns have shown no impact on the reported numbers.

Considering the margin front, there was an admirable 90 basis points sequential improvement in the operating margin, due to the cross-currency benefit (weakness of rupee partially negated by weak euro and British pound), operating efficiency, benefits of pyramid delivery (lower cost delivery by freshers), and lower sub-contracting. These benefits were slightly dampened by the higher establishment and travel cost. Surfing on improved utilization, efficient realization, execution rigour and the waning supply-side challenges in the second half, the company expects to hit an operating margin of 25 percent.

Company Viscera

The management of TCS has mentioned that they remain closely connected with the clients and have not seen a slowdown in budgets/deferral in spending/project cancellations etc.

The attrition figure of the last 12 months is 21.5 percent has improved to 19.7 percent in the preceding quarter, the management believes that attrition has peaked out and it should start falling. The management mentioned about the cooling off in the technology job market along with a fall in compensation expectations. This should provide a strong tailwind to margins.

Hiring has fallen with a net addition of less than 10,000. After a robust fresher hiring of 119,000 in FY22, the same is down to 35,000 in the first half (20,000 in Q2) of FY23. The company is looking to hire another 10,000 – 12,000 in the second half. This is not surprising in the light of the spare capacity and the tentative demand environment.

Outlook

The easing of supply constraints is relieving; however, the rocky macro environment might have some impact on demand. The macro uncertainty can slow down decision making and impact long-term project planning. The US appears to be fine currently, with minor loose ends in mortgage, insurance, discretionary retail etc. Europe may prove to be a mess due to the imminent threat of energy crisis which could impact industries. Finalizing, the future is complicated at this point of time.

If we look at the pre-pandemic valuation multiple, the stock was trading at 23.7x two-year forward earnings, almost similar to the current valuation. If macro turns more challenging, a temporary de-rating of valuation multiple is possible. Investors must capitalize on such weakness to accumulate the stock, given the promising long-term story. There is a decent downside support as the stock offers a very healthy pre-tax payout yield of close to 3 percent.

Technical Analysis

Let us look at the chart of TCS. The price has taken support at the 38.2% retracement level multiple times. We can assume that the operators are finding the Rs 3000 level to be a very emotional level. This level of 3000 has proven to be unbreakable on multiple instances.

We can observe a gap marked by a yellow box during October 2020 which indicates that the price might return to fill this gap. However, this gap filling might take a long time. The gap lies very close to the 61.8% retracement level. Investors can find the price of the stock of TCS around 2500 to be very attractive for accumulation in terms of long-term growth.

Currently MFI is 31 which indicates that the stock is hugely oversold, we cannot assert or predict the lows of this stock hence accumulation according to MFI close to 30 is a good indication. The stock price is below the 100 Day Moving Average. Therefore, it is a good time for accumulation of the stock of TCS.

Disclaimer: We do not endorse or encourage you to take trades or investment decisions based upon our posts/research, all of your trading and investment activities are your own and should be taken through consultation with reputed financial advisors. The analysis posted on this website has been created by involving multiple mediums which are present over the Internet.