Concor with its upcoming privatization of its business and finalization of dedicated freight corridors will aid the company for brilliant long-term prospects.

Highlights

Q1 volumes are led by domestic segment

New investment plans of over Rs 8000 crore in the next 4 years

Volume/revenue guidance for FY23 is retained at 10-12 percent

Margins are expected to remain stable over the next few quarters

Quarterly earnings results

The first quarterly results of Concor which is India’s largest container freight operator shows consistency in growth. The domestic business continued to display strong force, but the momentum in the EXIM (export-import) segment was slowed down by a tough macro environment.

Concor’s Q1 sales growth of 10 percent year on year was primarily led by higher realizations and a favorable base. Operating profit has risen by 9 percent YoY to Rs 479 crore as margins remained stable at 24 percent. Consolidated Net Profit after tax has increased by 15 percent to Rs 297 crore in comparison with the first quarter of the last year.

The EXIM volumes have dipped for the second consecutive quarter due to geopolitical uncertainties, non-availability of containers, and a lockdown in China (closure of major ports due to Covid-19). However, sustained demand momentum across the country boosted volumes in the domestic business, which have increased by 29 percent YoY. Overall volumes rose by 2 percent YoY as growth in the domestic segment was largely offset by weakness in the EXIM segment. Blended realizations grew 4 percent through higher lead distance and price hikes. Margins improved sequentially due to lower employee costs and other operating expenses.

Pending issue of LLF

During Q1 FY23, the company was accounted for LLF (Land License Fees) charges of Rs 96 crore. For the current fiscal year, the management has given a guidance of Rs 370 crore. The LLF payment for FY22 was slightly higher at Rs 450 crore as it included a one-time provision to the tune of Rs 70 crore. Meanwhile, the company is still in discussion with Indian Railways to convert the prevailing short-term lease to a single long-term lease of 30-40 years by making a one-time upfront payment.

Higher focus on bulk commodities

For FY23, the management expects healthy rise in domestic volumes. Also, it expects the EXIM business to rise by 10-12 percent in spite of a slow Q1. The company is looking to achieve a market share in bulk transportation of commodities. Concor has recently begun the transportation of bulk cement in containers. They are trying to add new rakes (80-tonne capacity) to accelerate the growth in bulk commodities.

Over the next 3-5 years, the company is planning an investment of Rs 8,000-10,000 crore to expand its distribution reach, infrastructure, containers, and equipment.

Technical Analysis

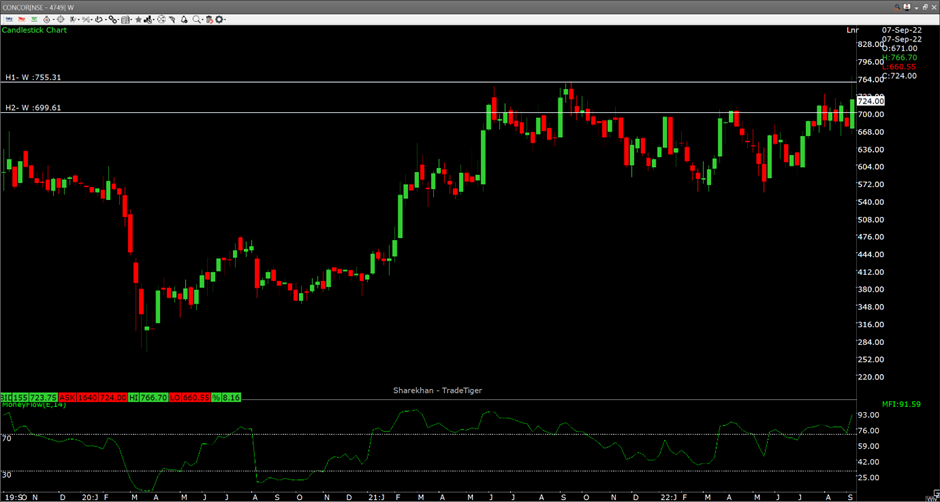

Let us observe the weekly candlestick chart of Concor:

Concor skyrocketed and hit the upper circuit of 10% on 7th September 2022. The stock soared up and achieved its lifetime high of Rs 766 as the company declared a 60% Final dividend for the financial year March 2022.

The stock is in the distribution zone. The price was severely rejected as the stock attempted for a breakout on 7th September 2022. MFI on weekly chart is at 91 which is an indication of the stock being immensely overbought.

A breakout over this zone will take the stock to new highs. New investments into this stock should be initiated only after corrections.

Outlook

Concor’s business has been quite tough despite the global economy has encountered a fundamental shift in the recent years. Geopolitical tensions, hiked oil prices, and high interest rates are eroding synchronized global growth. The EXIM volume decline in Q4 and Q1 suggests a weaker economic outlook.

The price of this stock has been consolidating in a wide range for the last 2 years and is now trading at 35 times FY23 estimated earnings. Investors may accumulate the stock on all corrections as long-term prospects appear bright due to the initiation of the dedicated freight corridor and the pending privatization of the business.