Sun Pharma has posted a brilliant result especially for the US specialty segment. A sequential growth in top line is clearly visible for most segments. Margins have improved which were aided by lower R&D expenses.

Sun Pharma posted a Consolidated Net Profit of Rs 2061 crore for the first quarter of this fiscal year on Friday 29th July 2022 which is a 42 per cent growth in comparison with the same quarter last year. Sun Pharma share price was up by 5% on Friday after the company posted their earnings results.

We are expecting a rise in the clinical trials which have been dampened by geopolitical developments and the fierce competition in the domestic diabetes market.

Specialty products – successive improvement

Sales of the specialty products were up by 29 per cent. They were driven by the force of Ilumya, Odomzo, Ceque and hampered by Absorica and Levulan. The company received higher performance from medical practitioners for the newly launched Winlevi for the treatment of acne vulgaris. They saw a progressive spike in the prescriptions for Winlevi.

Overall sales growth of 10.1 per cent was led by US formulations and emerging market businesses. The US formulations sales, which make up for 30 per cent of sales have grown by 10.7 percent.

The emerging market business which make up for 18 per cent of sales have grown by 12.6 percent.

Margins have slightly improved at gross level on a yearly basis.

Outlook

The company’s share of global specialty products (ex-Ilumya) has gained traction over the years and currently comprises of 13 percent of total sales which was 8 percent in FY18. The remarkable rise in prescriptions for Winlevi gives high hopes for the near term along with the force in other major specialty products.

The short-term challenge is for the clinical trials for Ilumya for the Japanese market. The Ukrainian war and regional developments have delayed these trials.

Considering the domestic business, the company owns the largest market share of 8.5 per cent. The company is investing to raise the field force and improve the quality of medical representatives. Their focus lies on dermatology, ophthalmology and oncology therapies.

The company’s major challenges in the coming months are defending against the high competition in the anti-diabetic segment. Sitagliptin is no longer patented which has caused the market to be flooded with multiple generic versions. However, Sitagliptin is not the ideal molecule for diabetes. Another class of drugs called as glifozins such as Dapagliflozin have emerged as the highly preferred alternative oral medicines.

The stock is trading at 17.3 times FY24e EV/EBITDA, which is well ahead of its peers.

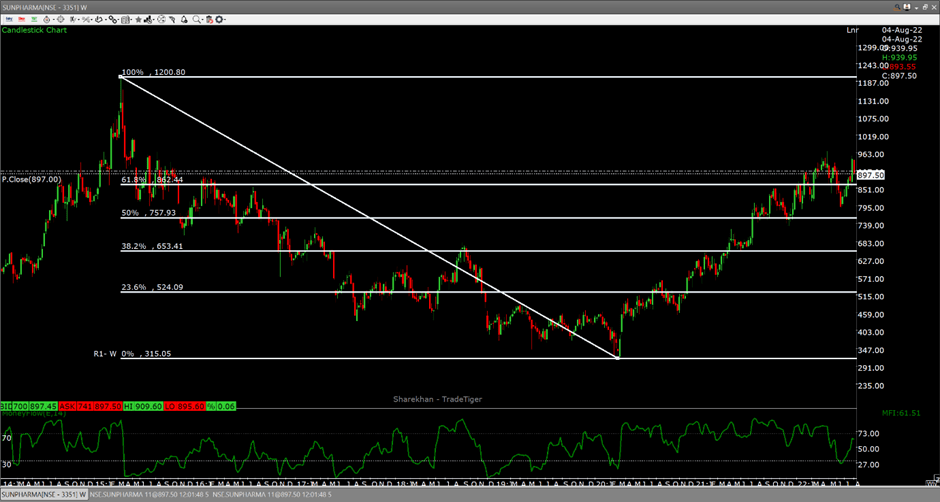

Let us take a look at the Weekly Candlestick Chart of Sun Pharma:

If we observe the retracement levels. The stock is struggling to achieve a breakout from the 61.8% retracement level. If the company continues with the consistency in the earnings for the coming quarters, we can expect the stock to have a breakout from the last retracement level and expect the price to rise up to its lifetime swing high of Rs 1200 which was achieved back in 2015.

MFI is 61 which shows the stock is not yet overbought, which is a good sign considering the chances of breakout have a high probability.

Disclaimer: We do not endorse you to take trades or investment decisions based upon our posts, all of your trading and investment activities are your own and should be taken through consultation with reputed financial advisors. The analysis posted on this website has been created by involving multiple mediums present over the Internet.