UPL Limited, previously known as United Phosphorus Limited, is an Indian multinational company which manufactures and markets agrochemicals, industrial chemicals, chemical intermediates, and specialty chemicals, and provides crop protection solutions. United Phosphorus Limited was established on 29 May 1969. The company renamed itself to UPL Limited in October 2013.

The company has their headquarters in Mumbai, Maharashtra, the company and it engages in both Agro and non-Agro activities. The Agro business is the company’s main source of income and includes the manufacture and marketing of conventional agrochemical products, seeds and other products required for agricultural. The non-Agro segment includes the manufacture and marketing of industrial chemical and other non-agricultural related products such as fungicides, herbicides, insecticides, plant growth and regulators, rodenticides, industrial and specialty chemicals, and nutri-feeds. UPL products are sold in over 150 countries.

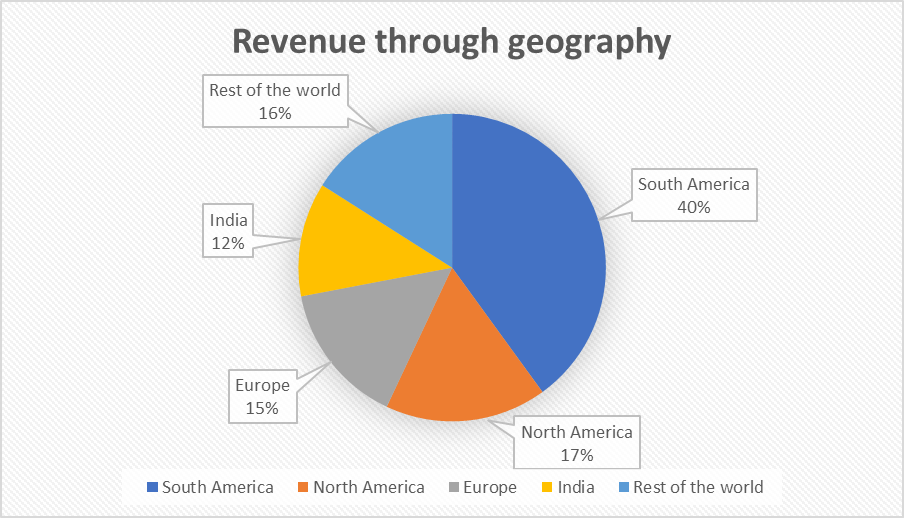

UPL Ltd is India’s biggest agrochemical company with a comprehensive product and services range for crop protection, seeds, bio-solutions and post-harvest products.

The first half of the current fiscal year continued to be vigorous without being affected by the challenging market conditions. The belief in a good rabi season in India and sturdy demand globally, as well as higher realizations on the back of a stronger product range would assist the company for a congruent performance in the second half.

Restructuring of the company

UPL, a short while ago, has undertaken corporate restructuring and parted their business into 4 unique segments — [1] India Agtech (crop protection & Digital) [2] Global crop protection (excluding India) [3] Global seeds [4] Manufacturing and specialty chemicals & others.

The company acquired renowned investors like ADIA, TPG, Brookfield and KKR to invest in the diversified segments and gained net proceeds of $260 million.

Long term panorama

During the first half of the current fiscal year, UPL has reported a revenue and EBITDA growth of 22 percent quarter on quarter (QoQ) and 31 percent year on year (YoY), which has been assisted by a stout rise in prices.

The company is planning to deploy 80 products in FY23 and owns a sturdy order book. Supported by its freshly initiation of the Flupyrimin insecticide, its new three-way mixture herbicide, as well as its NPP Biosolutions and seed treatment products for key rabi crops, the company is strongly assertive about a mid-single-digit volume growth and growth in market share gain in FY23.

The company has major alliances in the crop protection segment. It plans to raise set-ups across South-East Asia. It is vigorously investing in R&D and owns a product pipeline which has is valued greater than $5 billion.

UPL has stipulated its FY2027 objective of 10 percent per annum revenue growth for the long-term, and 15 percent per annum revenue growth for the Advanta seeds business. It plans to deploy six bio-based products and anticipates a growth CAGR of 20 percent in the bio-solutions segment by FY2027.

Prospect of Debt Reduction

UPL contemplates to produce cash flows of about $750 million in H2FY23 by means of working capital management. This would support in debt reduction of around $400 million.

The company has intentions to employ the net proceeds of $250 million from corporate restructuring for the purposes of debt repayment. Hence this would assist in reduction of its debt by $650 million.

UPL had acquired $150 million from share buyback in May 2022. The company expects a net debt reduction of ~$500 million by the end of FY23.

Technical Analysis

UPL stock price has been consolidated in the price range of Rs 625-850. The stock faces heavy resistance around its lifetime high of Rs 864 and has created multiple highs where the price has been rejected on multiple occasions. A breakout above the level of Rs 864 will take the stock higher. Currently, the price is taking support on the 38.2% retracement level. UPL appears to be a good candidate for directional neutral trading as per the Pathfinders Advance Options Course. The stock price is above the 200-day moving average which makes it relatively expensive for the mid-term. However, MFI is at 48 points which indicates a good buying opportunity. The stock might soon make a triple bottom around Rs 640 which might be a good entry point for long trades.

Disclaimer: We do not endorse or encourage you to take trades or investment decisions based upon our posts/research, all of your trading and investment activities are your own and should be taken through consultation with reputed financial advisors. The analysis posted on this website has been created by involving multiple mediums which are present over the Internet.