The oral care giant has notable strengths, it suffers into crucial areas which are sales, earnings growth and market share gains, which has ruined the share price.

Highlights

– Colgate’s persistent underperformance has been disappointing the investors, it has given a return of 60 percent in five years compared to the NIFTY FMCG gain of 75 percent

– A new CEO & MD Prabha Narasimhan who was previously in HUL, has been given the lead for ColPal in September. Now the spotlight rests on her. Will she drive the company into growth?

– Investors are highly concerned about the sales growth which currently feels like a snail

Reasoning

If the investors of ColPal had bet on the NIFTY’s FMCG stocks, they would have received a return of 75 percent over the past 5 years, however ColPal has given a mere 60 percent. The FMCG sector leader Hindustan Unilever has outperformed with a 200 percent return over 5 years.

Every underperforming stock has some reason to lag. If the operators are convinced that the company has settled the flaws or concerns, they will pump the stock. Consider ITC, the stock has soared after investors were convinced that punitive taxation and policy were no longer risks, and the pandemic-induced demand & destruction was temporary.

Colgate has a simple problem, low sales growth which cause erosion in its market share over the years. This leads to lower earnings growth. ColPal is a single-category company, dependent on oral care specifically toothpaste which is a high necessity category, as 90 percent of people are using toothpaste. Hence the market itself does not grow much and although Colgate has personal care as an additional category, it is not a significant area of focus.

Once ColPal and HUL were the main players, but Baba Ramdev with his Patanjali Ayurved made an aggressive and successful ayurvedic oral care push. Dabur India is prominent in oral care with its natural-focused range resulted in Colgate losing value. The chemical or white toothpaste market was very slow to wake up to the threat of Patanjali. The oral care market may not have grown fast, these two companies grabbed share from others. While the white toothpaste makers have launched their own herbal and ayurvedic variants, the balancing act has been a quite deteriorating because of growing one segment at the expense of the other.

Colgate has a convincing strategy to grow in the market. It has brands which cater to natural, herbal or the classic white toothpaste segments. Their variants that range from mass to premium. The strengths are into the kids segment, the association with dentists who promote the products to their patients. Also, Colgate has a wide distribution network and successful school-based marketing program. Its innovation rate is very healthy.

ColPal’s employee cost to sales is at 7.5 percent, which is higher than HUL’s 4.7 percent. Similarly, other expenses, as a percentage of sales, is higher at 16.4 percent compared to HUL’s 12.6 percent. The difference in scale means they are not precisely comparable, but some cost savings are possible. A better counterpart to cost cutting is improving the efficiency of all departments. But the reason for doing these should not be adding to margins, which are already healthy at Colgate at around 30 percent levels, but to invest in initiatives to accelerate sales growth.

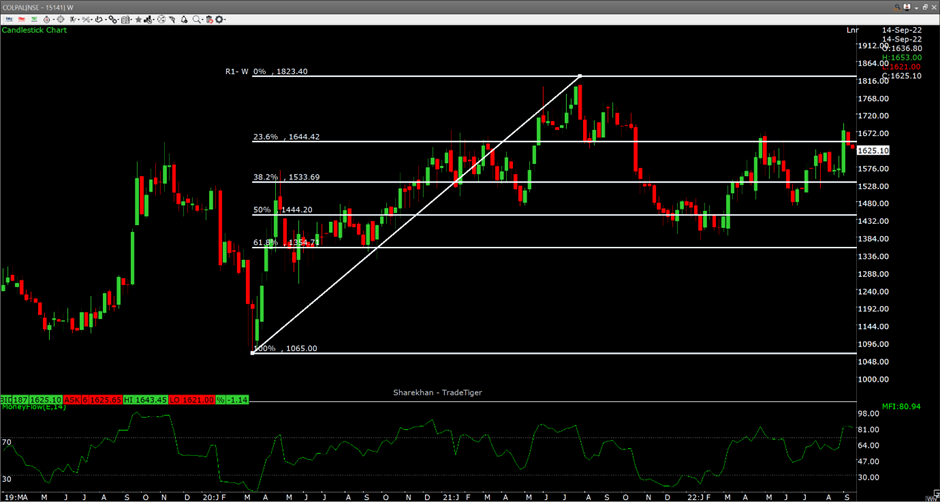

If we look at the recovery from the lows of the crash of 2020 to the recovery of 2021, ColPal has corrected due to Putin’s war in 2022. The stock has taken support at the 61.8% level as price was turned around multiple times. We may expect the stock price to rise to its lifetime high around 1800 to make a double top.

MFI is at 80 points which makes the stock highly overbought, it will face resistance as it rises further.

Outlook

Globally, Colgate is not dependent on oral care with other divisions such as pet care and personal care contributing significantly to sales. A bigger push into personal care could be a game changer in the long run although it may hit margins in the near term.

We cannot expect a quick turnaround in performance, as a change in business tactics will not be an easy task. A lot depends on the mandate given to Prabha by the board, guided by the parent company’s advice. She will benefit from the peaking of raw material and fuel prices which should bring some relief to cost cutting.

Disclaimer: We do not endorse or encourage you to take trades or investment decisions based upon our posts/research, all of your trading and investment activities are your own and should be taken through consultation with reputed financial advisors. The analysis posted on this website has been created by involving multiple mediums which are present over the Internet.